The Paperwork Crisis Comes for Orbit

Why the four preconditions for clearing house formation just aligned in space, and what gets built between now and 2028

Mitchell McLennan

Founder · Wavestar Holdings · May 14, 2026 · 22 min read

Author’s note. This piece is built around a single historical claim: every major central counterparty in the modern financial system was formed at the moment the same four preconditions aligned in its underlying market. Those preconditions just aligned in orbit, between January and May 2026. The piece is long because the case requires specificity; figures, dockets, names, and dates. Skim the bolded section claims if you are short on time.

1. A forty-billion-dollar trade nobody can settle

Claim: the orbital economy in May 2026 is mathematically and structurally identical to the Wall Street equities market in October 1968. The bilateral coordination model has reached its breaking point. The clearing layer has not yet been built.

Consider the trade.

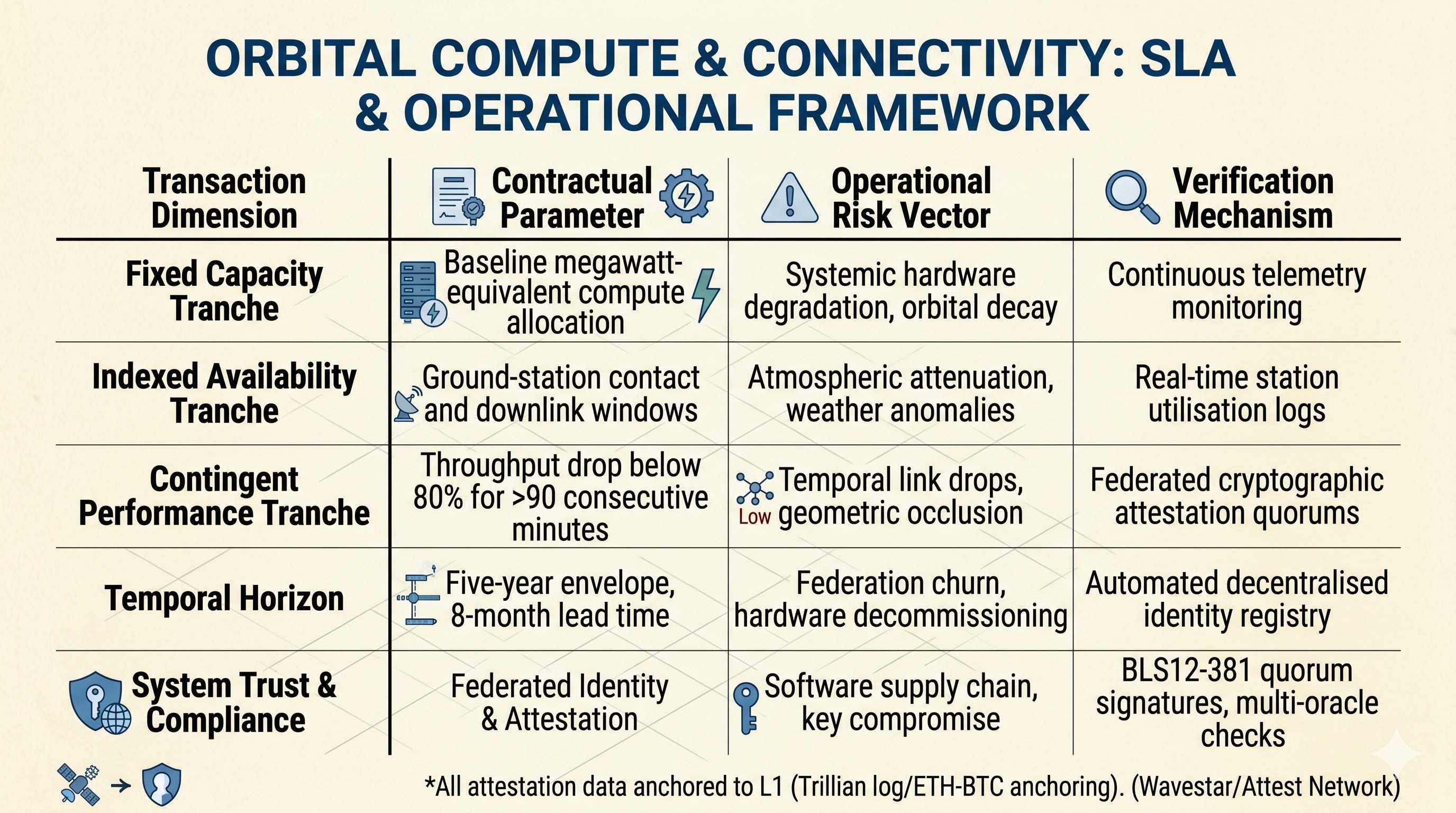

A frontier artificial intelligence lab commits to purchase roughly two hundred megawatt-equivalents of orbital AI compute capacity from a federation that includes SpaceX’s emerging orbital data-centre constellation and Starcloud’s GPU-equipped low Earth orbit satellites. The agreement is structured across a five-year envelope with three tranches; a fixed-price capacity tranche, an indexed tranche tied to real-time ground-station availability, and a contingent performance tranche that triggers if network downlink throughput from any participating orbital node falls below eighty percent of nameplate capacity for more than ninety consecutive minutes. The total notional is approximately forty billion dollars. The first delivery window opens in eight months. The buyer’s chief financial officer signs.

Now answer the operational questions in order.

Who is the legal counterparty on each leg of the trade once the federation membership shifts, which it will, as new operators integrate hardware and legacy satellites are decommissioned? Who anchors the audit trail of measured throughput during each delivery window in a way that the buyer’s auditors, the seller’s regulators, and the operators’ insurance underwriters will all accept? When an inter-satellite link drops for fourteen minutes inside a delivery window, who decides whether the contingent tranche triggers, and how is that decision proven later? If the largest operator inside the federation goes into capacity stress and is forced to deprioritise this contract for a higher-paying customer, who covers the buyer’s recourse before that operator’s other counterparties chain-react?

None of those operational questions has a default answer in May 2026. There is no neutral clearing house. There is no central counterparty. There is no shared identity registry that all the relevant operators recognise. There is no transparency log that the Federal Communications Commission, the Financial Crimes Enforcement Network, the Securities and Exchange Commission, and the Commodity Futures Trading Commission could reach in parallel. There are bilateral contracts, side letters, and an implicit assumption that the largest operator in the federation will absorb the operational and financial cost of any failure mode that public-facing reputation cannot tolerate. That assumption is the orbital equivalent of the Wednesday closings on the New York Stock Exchange in 1968, when paper certificates physically clogged Wall Street back offices and the industry’s response was to stop trading one day a week so clerks could catch up.

Take-away. The orbital economy is now trading instruments that look like 1990s wholesale electricity contracts and 1960s OTC equity blocks at the same time; heterogeneous, time-bounded, indexed, federated, and high-velocity. The financial infrastructure to clear, anchor, and settle them does not exist. Building it is what Wavestar is for.

2. The four preconditions for clearing-house formation

Claim: every major central counterparty in the modern financial system was formed at the moment four preconditions aligned in its underlying market. Those preconditions just aligned in orbit.

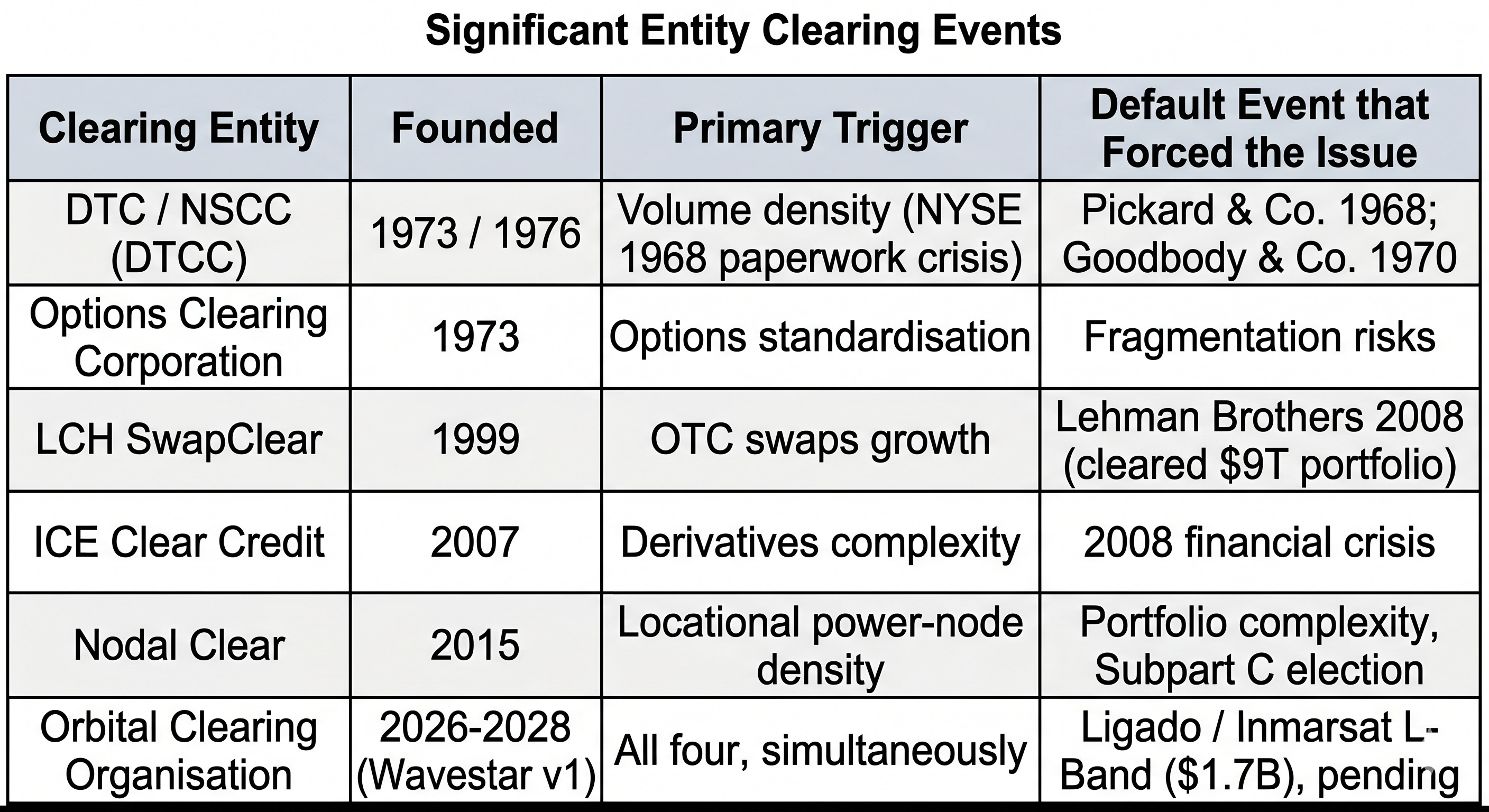

A historical review of clearing-house formation reveals a consistent pattern. The Depository Trust Company (1973), the National Securities Clearing Corporation (1976), LCH SwapClear (1999), Nodal Clear (2015), and ICE Clear Credit (2007) were all formed at the same structural inflection. Volume density crossed the threshold at which bilateral settlement physically failed. The asset class crystallised into something standardised enough to clear. The regulatory environment shifted from permitting bilateralism to demanding central oversight. And a forcing-function default exposed the fragility of the existing model.

The sections that follow walk through each of the four preconditions, with the 2026 orbital data. The conclusion is not subtle. The market has crossed all four lines.

3. Precondition one: volume density has reached the 1968 threshold

Claim: the satellite population, launch cadence, and bilateral deal flow in 2026 mirror, in structural terms, the NYSE volume that triggered the 1968 paperwork crisis. The back-office work of orbit; spectrum coordination, conjunction assessment, interference mitigation; can no longer be carried by bilateral private negotiation.

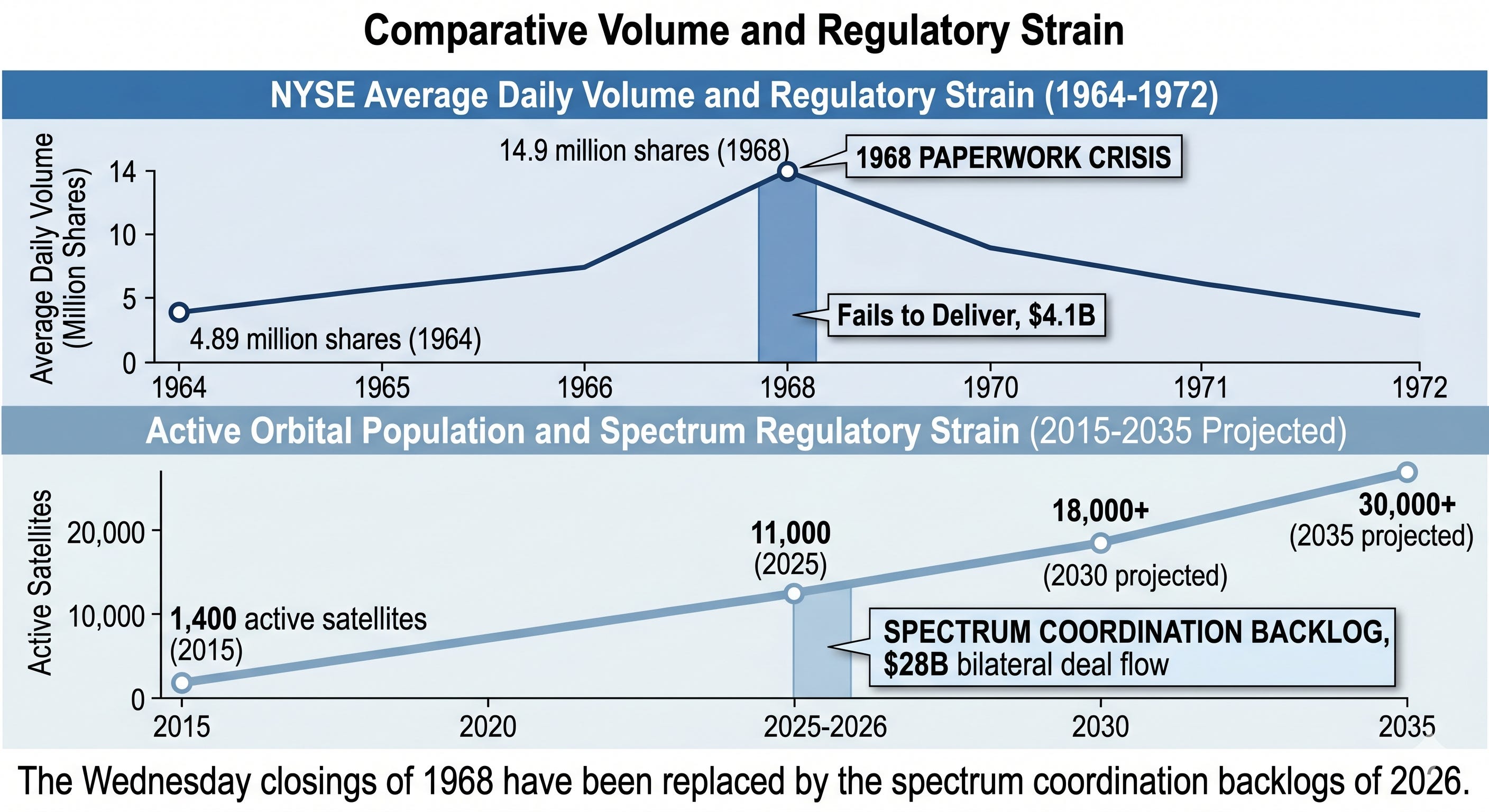

In 1964 the New York Stock Exchange traded an average of 4.89 million shares per day. By 1968 the average had reached 14.9 million, and the daily volume record set in 1929 was broken twenty-four times in that year alone. The transaction processing system, still operating on paper certificates that passed through as many as one hundred pairs of hands per trade, broke. Fails to deliver peaked at approximately $4.1 billion. The NYSE began closing on Wednesdays so clerks could process the backlog. Trading days were shortened. The settlement period was extended from four to five days. Two member firms collapsed: Pickard & Company in May 1968, then Goodbody & Company in October 1970, with the Goodbody failure costing the NYSE trust fund $21 million and serving as the final political push for the Central Certificate Service to evolve into the Depository Trust Company.

The orbital population curve is steeper.

In 2015 there were approximately 1,400 active satellites in space. By 2025 the figure exceeded 11,000. Novaspace’s 2026 outlook for the small-satellite market projects 16,900 small satellites (under 500 kg) launched in the 2026-2035 envelope, equating to roughly 230 tons of orbital hardware deployed per year, with serial-production facilities such as India’s Azista BST targeting two satellites per week. By 2030 the active population is projected at 18,000 or more, and by 2035 at over 30,000.

The financial flow is comparably steep. In April 2026 FCC Chairman Brendan Carr noted that modernising spectrum sharing under Report and Order DOC-421308A1 (SB Docket 25-157) could unlock more than two billion dollars in direct economic benefits, and disclosed approximately twenty-eight billion dollars in bilateral spectrum deal flow over the preceding eighteen months, much of it tied to direct-to-device and next-generation satellite broadband.

The volume-density precondition is satisfied. The “Wednesday closings” of 1968 have been replaced by the spectrum coordination backlogs and bilateral side letters of 2026.

4. Precondition two: the orbital asset class just crystallised

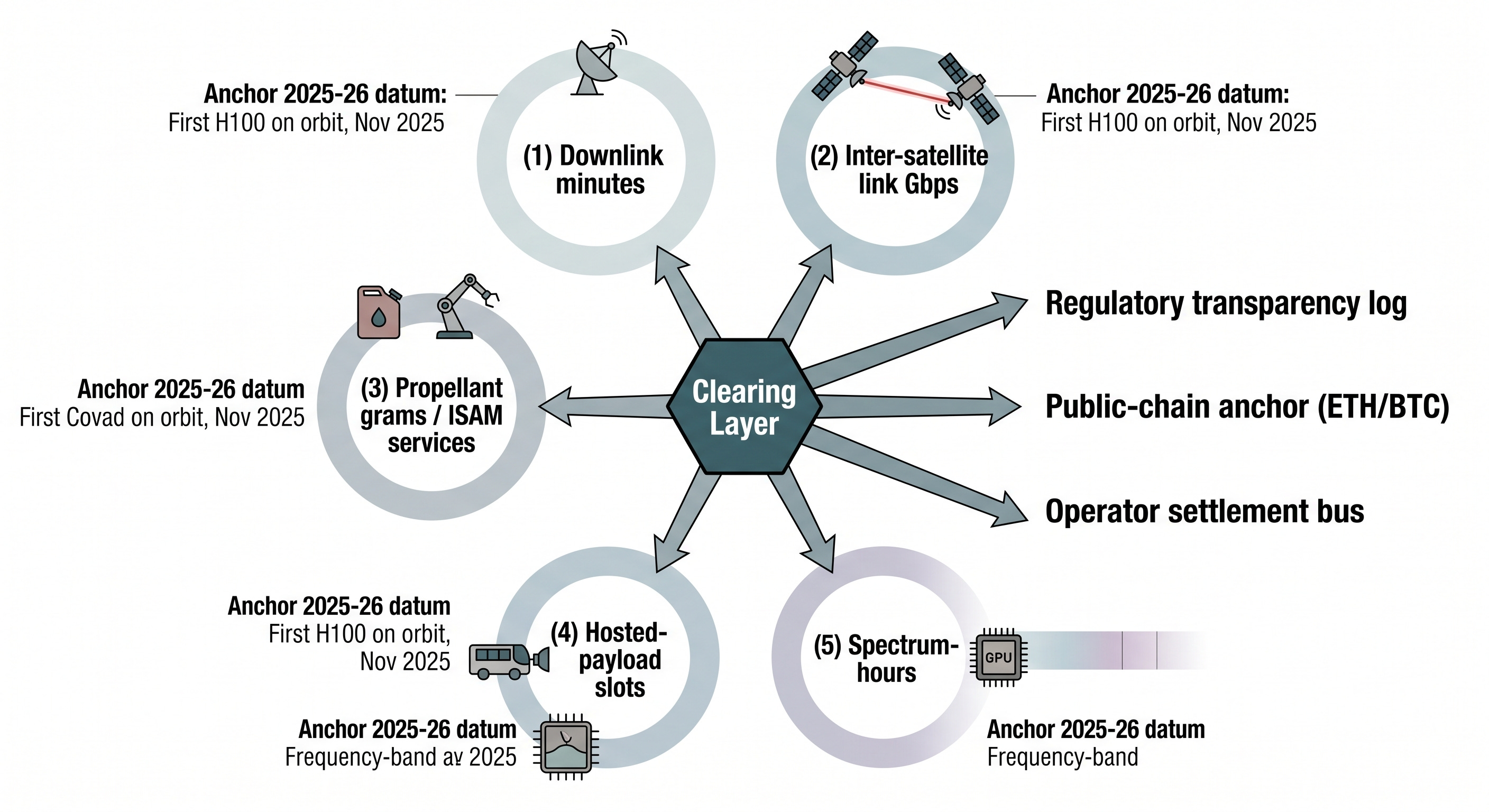

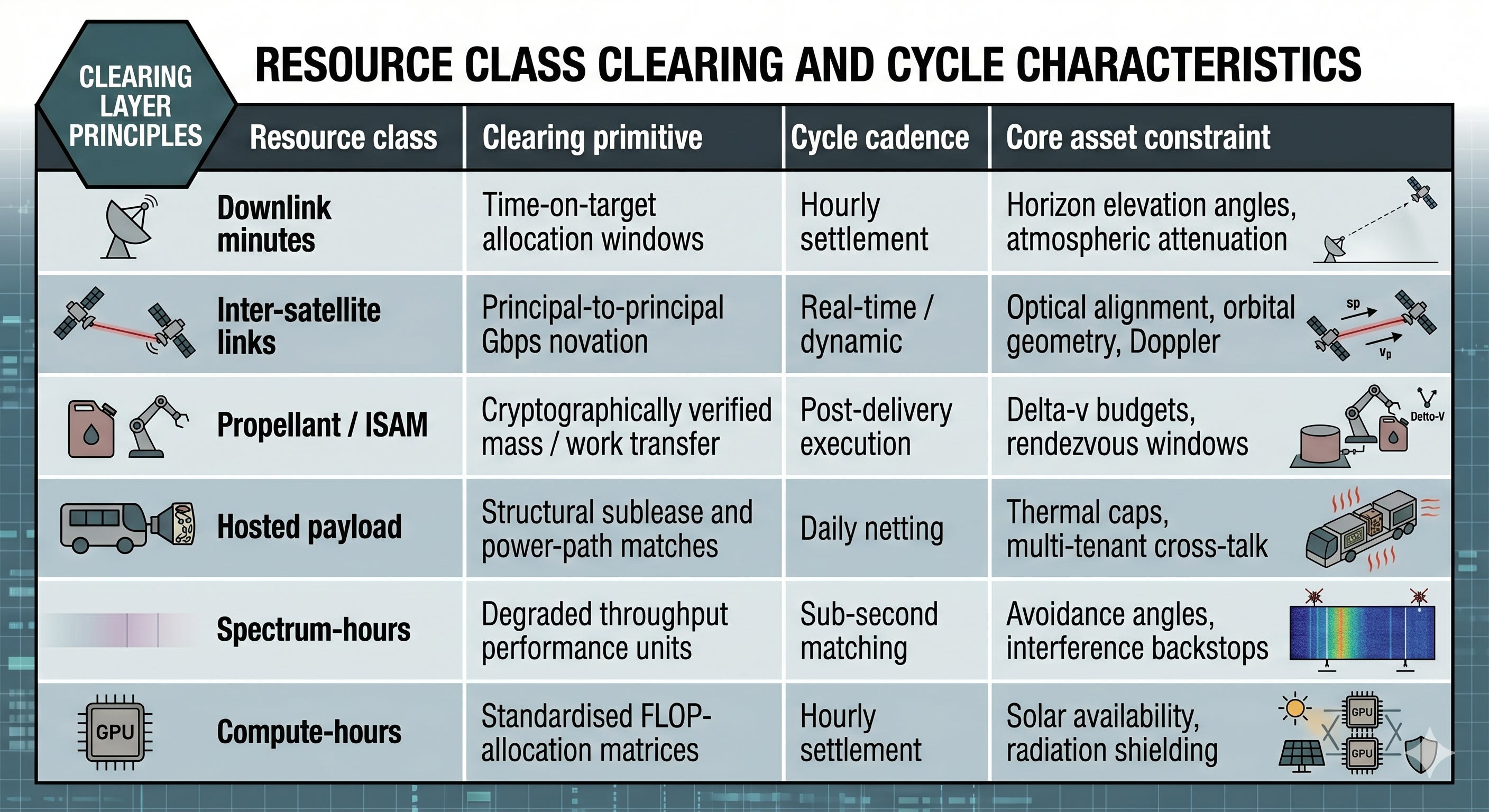

Claim: the orbital economy has six distinct resource classes, each with its own physics, each now standardised enough to clear. The crystallisation happened in the last eighteen months.

The asset class is what was missing. Until late 2025, orbital resources were enumerated by engineers, not by markets. That has now changed in each of six segments.

Downlink minutes are time-bounded windows of ground-station contact at specified radio-frequency bands and elevation angles. The underlying physics is well-defined and minutes-on-target are directly measurable, which makes downlink the most standardised derivative in the orbital economy. Earth station licensing and coordination filings overseen by the Federal Communications Commission Space Bureau put downlink under regulatory clearing pressure first.

Inter-satellite link capacity is the backbone of LEO megaconstellation economics. The January 2026 launch of Kepler Communications’ first Aether tranche of optical relay satellites is the moment ISL capacity crystallised into a tradeable asset. Aether terminals are compatible with US Space Development Agency optical standards, ensuring interoperability between commercial and government constellations, and the network is marketed as a managed service with defined service-level agreements; effectively a tradable data-transport layer in orbit. Each Aether satellite includes multi-GPU compute modules and terabytes of storage, blurring the line between transport and compute.

Propellant grams and in-space servicing, assembly and manufacturing (ISAM) services represent the youngest physical asset class. The Government Accountability Office’s July 2025 report on ISAM flagged a chicken-and-egg problem; providers and users hesitant to commit without proven standards or a government champion. Orbit Fab and Starfish Space are now defining the operational standards. Failure modes in this class are physical: thrust deficits, rendezvous synchronisation misses, unverified mass delivered. Clearing requires empirical physical measurement, not abstract ledger accounting.

Hosted-payload slots behave economically like commercial real estate. The asset bundle is the structural bay plus the thermal dissipation budget plus the power path plus the downlink. The February 2026 award to AST SpaceMobile under the Space Development Agency HALO Europa programme; a thirty-million-dollar prime contract to demonstrate resilient tactical communications directly through the BlueBird constellation; established hosted-payload-as-a-service as a defence-procurement category, not just a commercial one. Wavestar Market operates as the multiple-listing-service equivalent for this segment.

Spectrum-hours were not a tradeable asset class in the United States before 30 April 2026. The FCC’s adoption of Report and Order DOC-421308A1 (SB Docket 25-157) on that date is the regulatory unlock that turned spectrum-hours into a clearable commodity. The next section covers the order in detail.

Compute-hours are the youngest and the most capital-intensive class. Starcloud-1, a 60-kilogram satellite launched on a SpaceX rocket in November 2025, integrated the first space-qualified NVIDIA H100 GPU and achieved a one-hundredfold increase in on-orbit processing power versus legacy space hardware. By December 2025 the platform had executed a localised Gemini model and trained the first large language model in space, running Andrej Karpathy’s nanoGPT architecture entirely on orbit. Starcloud’s leadership team is the kind of institutional cross-pollination that makes the asset class credible: CEO Philip Johnston, a former McKinsey satellite-systems specialist with advanced degrees in mathematics, national security and business administration and a CFA charter; CTO Ezra Feilden, a materials engineer with a doctorate from Imperial College London who specialised in deployable solar structures at Airbus Defence and Space; and Chief Engineer Adi Oltean, a former SpaceX and Microsoft engineer holding twenty-five patents in machine-learning infrastructure and satellite networking. Starcloud closed a one-hundred-seventy-million-dollar Series A at a one-point-one-billion-dollar valuation led by Benchmark in March 2026. Starcloud-2 scales localised power generation by a factor of one hundred and is scheduled for sun-synchronous deployment in late 2026.

The asset-class-definition precondition is satisfied.

5. Precondition three: the regulatory permission curve just inverted

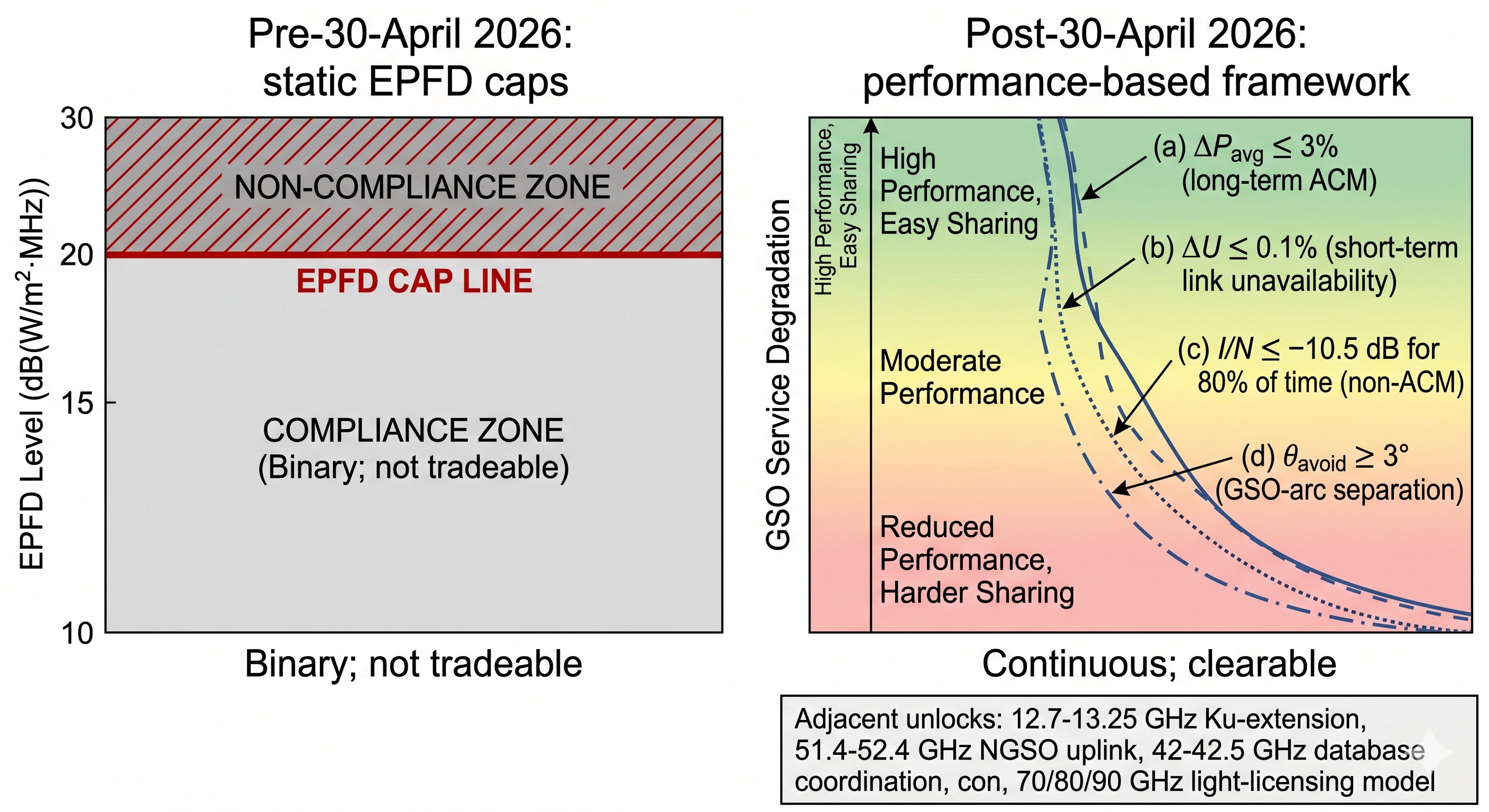

Claim: between April and March 2026 the United States regulatory environment moved from permitting bilateralism to demanding central oversight. The two load-bearing instruments are the FCC’s April 30 order and the SEC / CFTC March 11 Memorandum of Understanding.

On 30 April 2026 the FCC adopted Report and Order DOC-421308A1 under SB Docket 25-157 and rewrote the framework that has governed NGSO and GSO spectrum coexistence since the 1997 International Telecommunication Union regime. The legacy Equivalent Power Flux Density limits were a binary step-function; either an NGSO operator’s emissions stayed under a fixed mask at the geostationary arc, or the operator was denied operational authority. The FCC replaced that with a continuous, performance-based coordination framework. The agency adopted 328 reference GSO links as benchmarks and imposed four numerical backstops:

The long-term GSO protection threshold for networks using adaptive coding and modulation:

The short-term interference threshold, capping any absolute increase in link unavailability at:

For GSO networks not using ACM, an interference-to-noise ratio backstop:

And, on the geometric side, a minimum NGSO avoidance angle relative to the visible geostationary arc:

Each of these thresholds is a continuous variable. That is the structural change.

The order also opened the 12.7-13.25 GHz band as a Ku downlink extension, allocated the 51.4-52.4 GHz band for NGSO uplink operations, and established automated database coordination in the 42-42.5 GHz band modelled on the light-licensing framework that has worked in the 70/80/90 GHz bands. Each of those allocations creates additional bands that can be priced and traded.

The closest historical parallel is FERC Order 888 in 1996, which mandated open, non-discriminatory access to the US electrical transmission system. Order 888 did not create the wholesale electricity market; it created the conditions under which the market could form. The clearing infrastructure (the regional ISOs and RTOs; PJM, MISO, NYISO, CAISO, ISO-NE, ERCOT) was then built between 1998 and 2002 and went on to clear trillions in derivatives annually. The FCC’s 30 April order plays the same structural role for orbital spectrum.

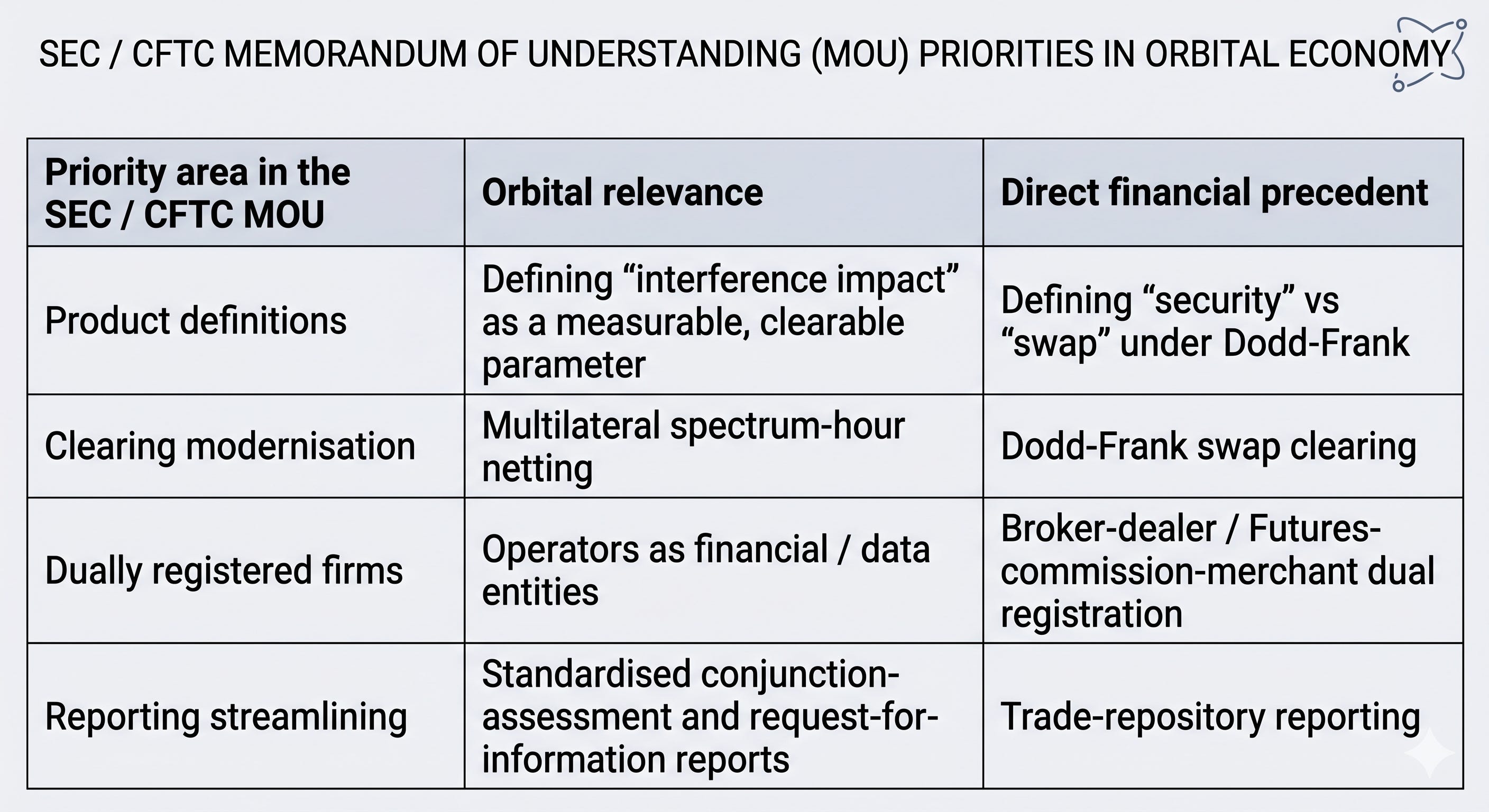

The second instrument matters because clearing is multi-agency. On 11 March 2026 the Securities and Exchange Commission and the Commodity Futures Trading Commission published a Memorandum of Understanding establishing a Joint Harmonisation Initiative. The MOU explicitly aims to reduce regulatory turf wars, to harmonise product definitions, and to coordinate clearing modernisation; it adopts what the agencies are calling a “minimum effective dose” approach to regulation. One of the six listed priority areas is modernisation of clearing, margin, and collateral frameworks.

The regulatory-permission precondition is satisfied. The agencies with jurisdiction over orbital clearing (the FCC for spectrum, FinCEN for money transmission, the SEC for any security-like wrapper, the CFTC for derivatives) have, between March and April 2026, opened a coordinated regulatory pathway for the first time.

6. Precondition four: the forcing-function default is already on the books

Claim: every modern clearing house was forced into existence by a counterparty failure that exposed the fragility of bilateralism. The orbital equivalent is the Ligado / Inmarsat L-Band crisis, with the FCC’s DISH / EchoStar escrow order as the reinforcing precedent.

In financial history clearing houses are formed in the wake of default shocks. The Goodbody & Company collapse in October 1970, costing the NYSE trust fund twenty-one million dollars, was the political push that turned the Central Certificate Service into the Depository Trust Company. LCH SwapClear’s 2008 success in unwinding Lehman Brothers’ nine-trillion-dollar interest-rate-swap portfolio without taxpayer assistance was the moment OTC central clearing went from optional to mandatory. ICE Clear Credit was founded in the same year for the same reason. The forcing-function pattern is consistent.

The orbital equivalent is unfolding now, in two parts.

The first is the Ligado / Inmarsat (now Viasat) L-Band Cooperation Agreement. The original 2007 agreement, amended in 2010, was a massive bilateral bet on spectrum sharing in the L-Band; the financial value of the agreement is publicly disclosed at approximately $1.7 billion. The failure of Ligado (formerly LightSquared) to realise its terrestrial network plans, combined with ongoing bankruptcy court proceedings, has produced significant financial distress for both parties. Viasat’s fiscal 2024 results included integration overhead from the Inmarsat acquisition and a $770 million insurance claim covering the Viasat-3 Flight 1 and Inmarsat-6 F2 satellite anomalies. The litigation chains are now interleaved across multiple courts. None of this would have happened under a central counterparty.

The second is the FCC’s May 2026 requirement, in the DISH / EchoStar context, for a $2.4 billion escrow account to address obligations owed to contractors and tower owners. The agency’s intervention is itself an admission that bilateral arrangements in the satellite-spectrum sector are now systemically fragile enough to require federal collateral mechanisms ad hoc. That is exactly the kind of pre-CCP emergency intervention that, in 1968 and 1970, preceded the formal creation of central clearing.

The forcing-function-default precondition is satisfied, in advance of a larger cascade. The historical pattern says the cascade comes. The architectural question is what is in place when it does.

7. The architectural question: DTCC, LCH, or Nodal Clear?

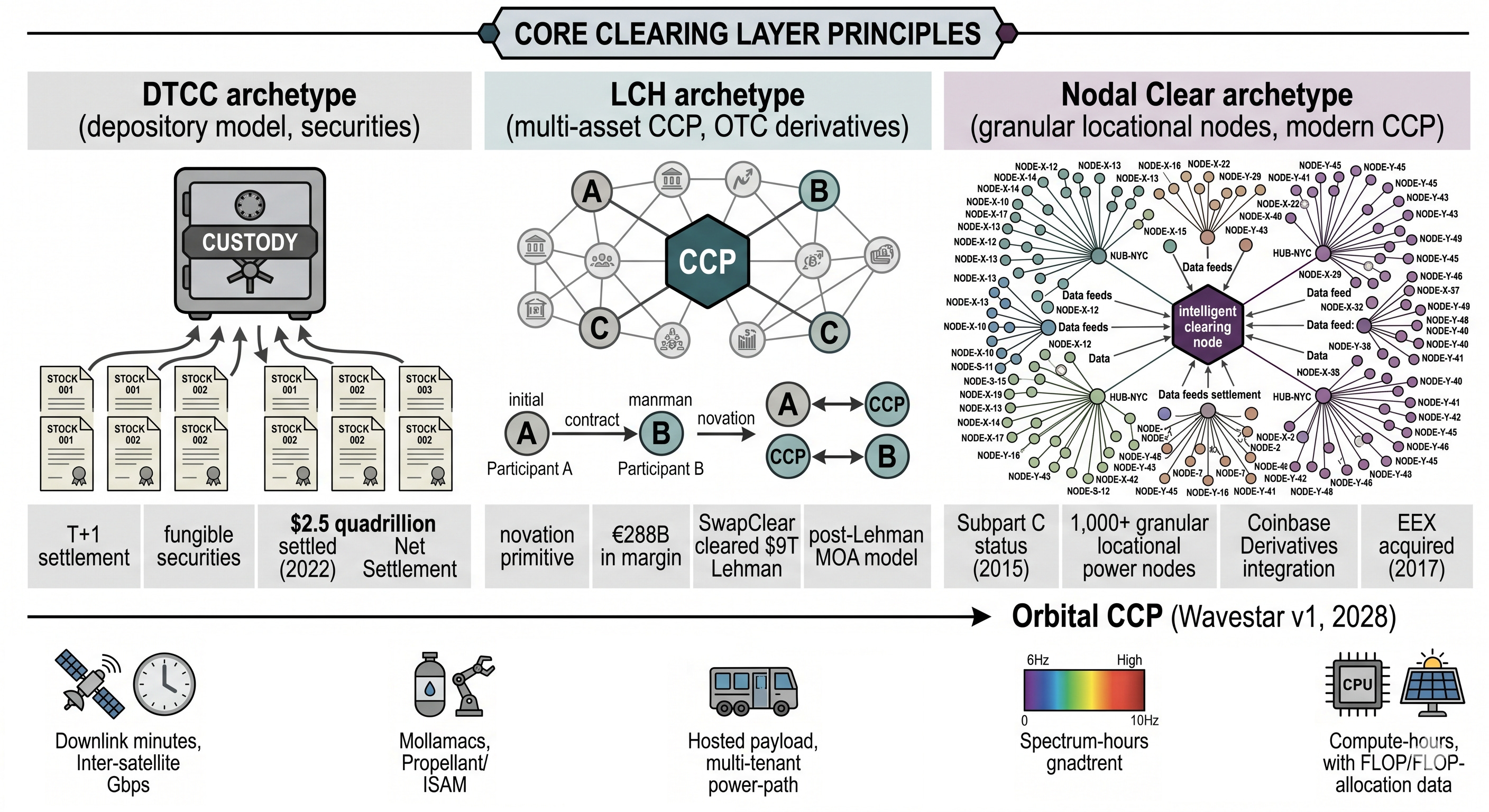

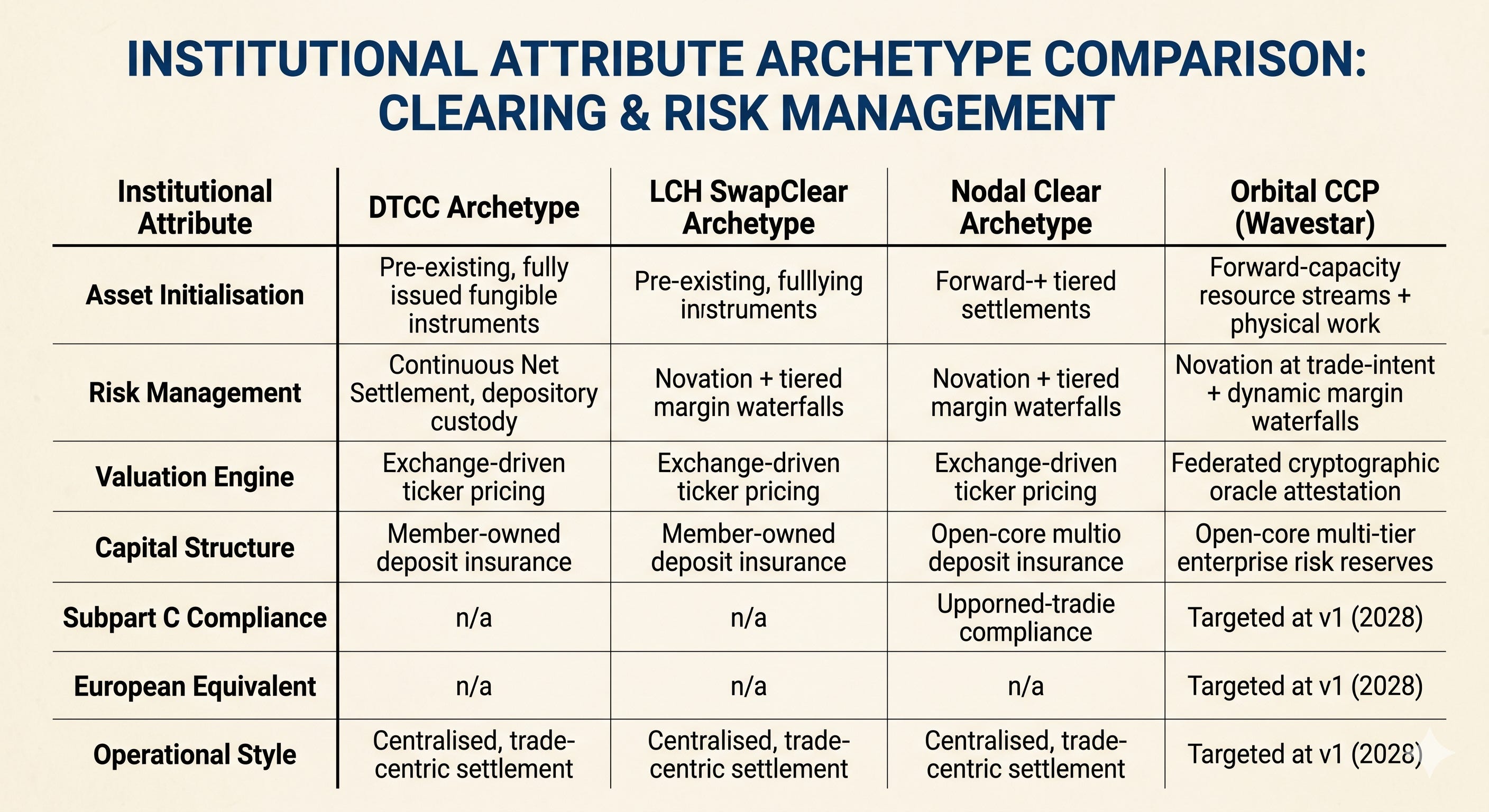

Claim: orbital trades are heterogeneous, time-bounded, locationally-specific, and frequently do not exist at the moment of agreement. The clearing primitive is novation, not depository custody. The most precise modern analog is not DTCC and not LCH SwapClear; it is Nodal Clear.

The popular shorthand is “DTCC for space.” That phrasing is intuitive and structurally wrong.

DTCC’s Depository Trust Company subsidiary holds book-entry records of US securities already inside the system. Its National Securities Clearing Corporation subsidiary then clears broker-to-broker trades against that depository via Continuous Net Settlement. The mechanism is beautifully optimised for one specific job; high-volume, identical-asset, T+1 settlement of fungible securities whose ownership is already in custody. Every part of that sentence is doing work. “High-volume” is what makes CNS netting tractable. “Identical-asset” is why a thousand shares of Apple is interchangeable with any other thousand. “T+1” means the temporal mismatch is small. “Fungible” means book-entry custody is meaningful. “Already in custody” means the asset existed at the moment of trade. DTCC settled approximately $2.5 quadrillion in value in 2022, the highest financial value processor in the world.

None of those assumptions apply to orbital resources. A downlink minute over Svalbard at 09:42 UTC at 47.6 degrees of elevation is not interchangeable with a downlink minute over Mauritius at 09:43 UTC at 23 degrees; the asset is non-fungible. Most orbital resources do not exist at the moment of trade; the satellite has not yet reached the relevant orbit, the spacecraft has not yet performed the manoeuvre, the spectrum window has not yet opened, the GPU has not yet seen sunlight. The temporal mismatch between trade and delivery is not T+1; it ranges from minutes to years. The asset cannot be held in custody; it can only be measured at delivery.

LCH (London Clearing House, now part of the LSEG group) is the multi-asset, multi-currency CCP that makes the right structural argument. LCH operates across complex over-the-counter asset classes through specialised SwapClear and RepoClear systems. The legal primitive is novation; at the moment a bilateral trade intent is validated, the CCP legally dissolves the original contract between the buyer and seller and replaces it with two distinct principal-facing agreements (buyer-CCP and CCP-seller). The CCP does not need to own the underlying asset; counterparty default risk is collateralised through real-time margin posting and structured default waterfalls, supplemented by mutualised default funds. LCH held approximately €288 billion in margin collateral as of October 2024. In 2008 LCH SwapClear unwound roughly $9 trillion in interest-rate-swap exposure to Lehman Brothers without taxpayer assistance, an operation that went largely unnoticed in the wider press precisely because the CCP model worked as designed.

For orbital settlement the architectural argument is stronger than LCH, however. The closest modern analog is Nodal Clear.

Nodal Exchange and its clearing subsidiary Nodal Clear were founded in 2009 and registered as a Derivatives Clearing Organisation in 2015, electing Subpart C status at registration; the first DCO to do so. Subpart C status requires adherence to the Principles for Financial Market Infrastructures and enables third-country recognition by the European Securities and Markets Authority. Nodal’s distinguishing technical feature is that it clears more than one thousand granular locational power nodes, where prices are settled based on specific physical constraints unique to each node. That structure (granular, location-specific, physical-constraint-bound, with a Subpart C regulatory wrapper) is the closest existing analog to what an orbital clearing organisation has to be. In 2017 the European Energy Exchange acquired Nodal, demonstrating that locational utilities are absorbed into global exchange groups once their clearing function matures. In 2022 Nodal Clear began clearing for Coinbase Derivatives, proving the same architecture handles high-velocity digital products alongside physical commodity futures.

Wavestar is the orbital-specific application of the Nodal Clear architectural pattern, extended for non-fungible time-bounded resources that do not yet exist at the moment of trade.

8. The architecture

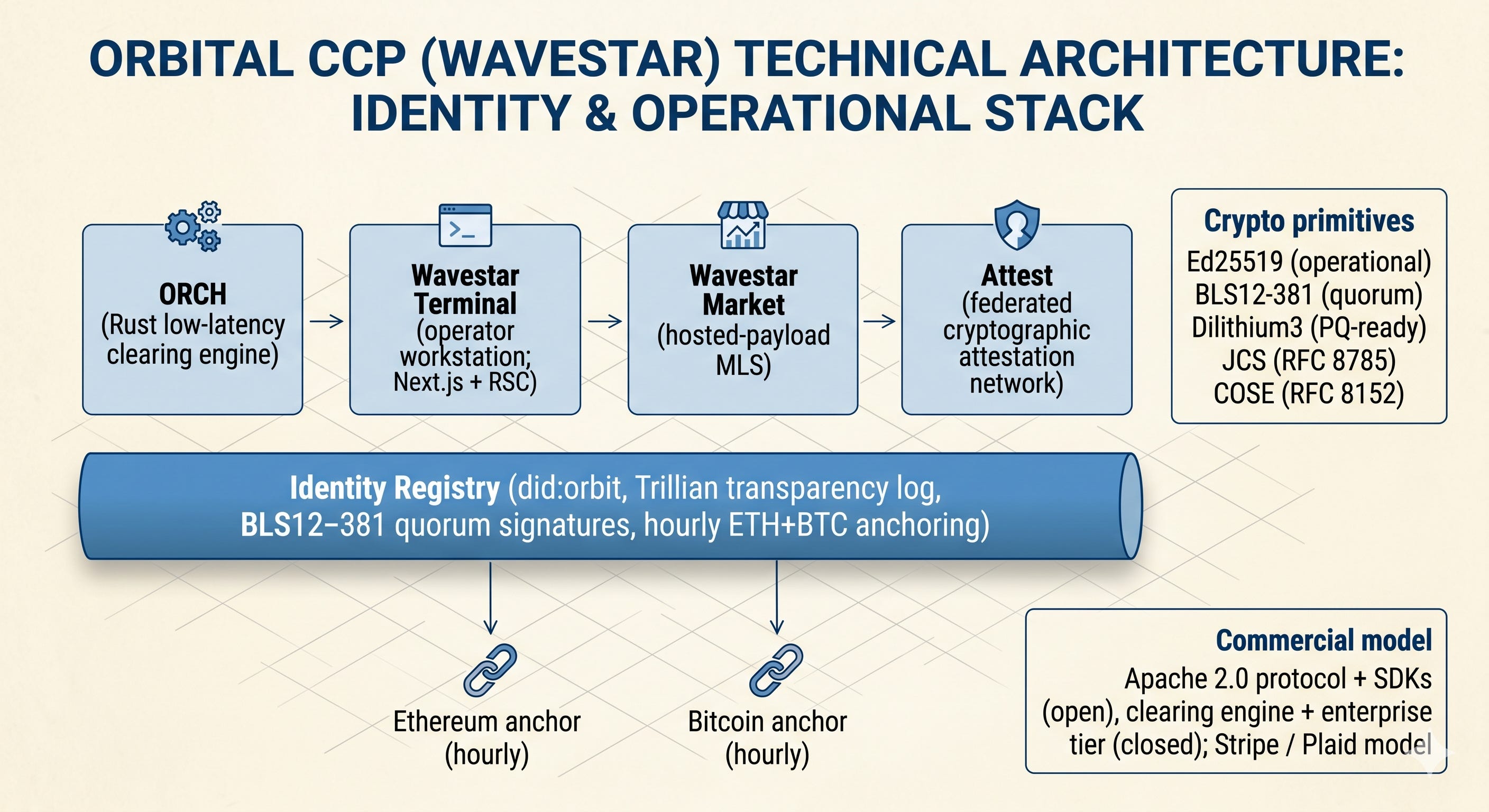

Claim: a four-module application suite on a shared identity-registry spine is the minimum viable shape for a neutral orbital CCP. The crypto primitives are vetted. The technical risk is in productisation, not invention.

The four modules.

ORCH is the clearing engine, Rust-implemented for low-latency matching and novation. ORCH ingests multi-party trade intents, becomes principal counterparty via novation at the moment of trade, manages margin posting and default waterfalls, and executes settlement at the cadence appropriate to each instrument; sub-second for spectrum-hour intraday matching, hourly for downlink minute futures, daily for hosted-payload netting, post-delivery for ISAM mass / work transfers.

Wavestar Terminal is the operator system of record. The shorthand is “Bloomberg for orbit”; a single workstation showing the operator their open cleared positions across all six resource classes, their counterparty credit exposures, their margin requirements, and their forward delivery calendar. Built on Next.js with React Server Components.

Wavestar Market is the multiple-listing-service equivalent for hosted-payload capacity. It is the discovery layer for the segment with the slowest inventory and the most complex tenant-mix economics, and the segment where neutral discovery infrastructure delivers immediate commercial value to both sides.

Attest is the federated cryptographic attestation network for orbital facts; ephemeris vectors, telemetry logs, ground-station performance metrics, ITU SNS filings, FCC IBFS filings. Any external fact used in a settlement decision in ORCH must first be signed by an Attest quorum using BLS12-381 aggregation. The output is a signed claim that ORCH can use without further verification.

All four sit on a shared spine: an identity registry using the did:orbit: DID method (an open W3C-extension specification we are proposing), backed by a Trillian-based Merkle transparency log, anchored hourly to both Ethereum and Bitcoin for tamper-evidence.

The crypto primitives are vetted, not novel: Ed25519 for operational signatures, BLS12-381 for quorum aggregation, Dilithium3 wired in but not default so the protocol can flip to post-quantum signatures without breaking the clearing API, RFC 8785 (JCS) for canonicalisation of any signed payload, RFC 8152 (COSE) for envelopes crossing module boundaries.

The commercial structure is the Stripe / Plaid model. The protocol and SDKs are Apache 2.0; the clearing engine and the enterprise tier (compliance reporting, regulatory dashboards, margin analytics) are closed source. Operators, integrators, and the open-source community can build on the spec without licensing it. Wavestar makes money from the clearing flow and the enterprise tier.

This architecture is not isolated from the broader orbital-validation ecosystem. Orbit AI’s Genesis mission in December 2025 validated on-orbit blockchain node operations and transaction verification integrated with real-time edge computing. Decentralised IoT identity systems using lightweight Directed Acyclic Graph structures over the Shimmer testnet handle device verification within short satellite visibility windows. Permissioned architectures such as InsureConnect already use DIDs, verifiable credentials, and off-chain IPFS data storage to record multi-party contracts and tracking data. Wavestar interoperates with these by design; the registry layer is the integration surface.

9. Counter-arguments: who else could clear this, and why none of them will

Claim: the existing candidates for orbital clearing all stop short of central counterparty status. The Space Data Association is a flight-safety utility, not a CCP. CME’s weather derivatives suite is structurally constrained to ten percent of the underlying weather-risk market. The new “orbital orchestration” cohort builds the technical layer below the CCP, not the CCP itself.

A serious case requires engaging the counter-positions seriously. There are three.

The Space Data Association. Founded in 2009 by SES, Intelsat, and Inmarsat, the SDA handles flight-safety data sharing among major satellite operators. The organisation’s recent conjunction-assessment mining shows that close approaches in LEO are now occurring five times more often than in 2018, a structural data point in its own right. However, SDA’s charter explicitly prohibits use of its data for commercial purposes such as sales, planning, or marketing. The body sees itself as a bridge to public paradigms like the US Department of Commerce’s TraCSS. SDA is therefore a flight-safety utility, not a clearing utility, and the governance constraint is structural, not technological.

CME’s weather derivatives suite. CME launched the weather contracts in 1999 and the segment has grown substantially recently; average trading volumes surged 260% in 2023. However, exchange-traded weather derivatives still represent only around ten percent of the total twenty-five-billion-dollar weather-risk market; the remaining ninety percent is in bilateral OTC. The structural lesson is that CME’s product can survive in adjacent commodity classes but cannot, by its instrument design, become the central counterparty for a non-financial physical risk class. The orbital analog argues for a purpose-built CCP, not a CME wrapper.

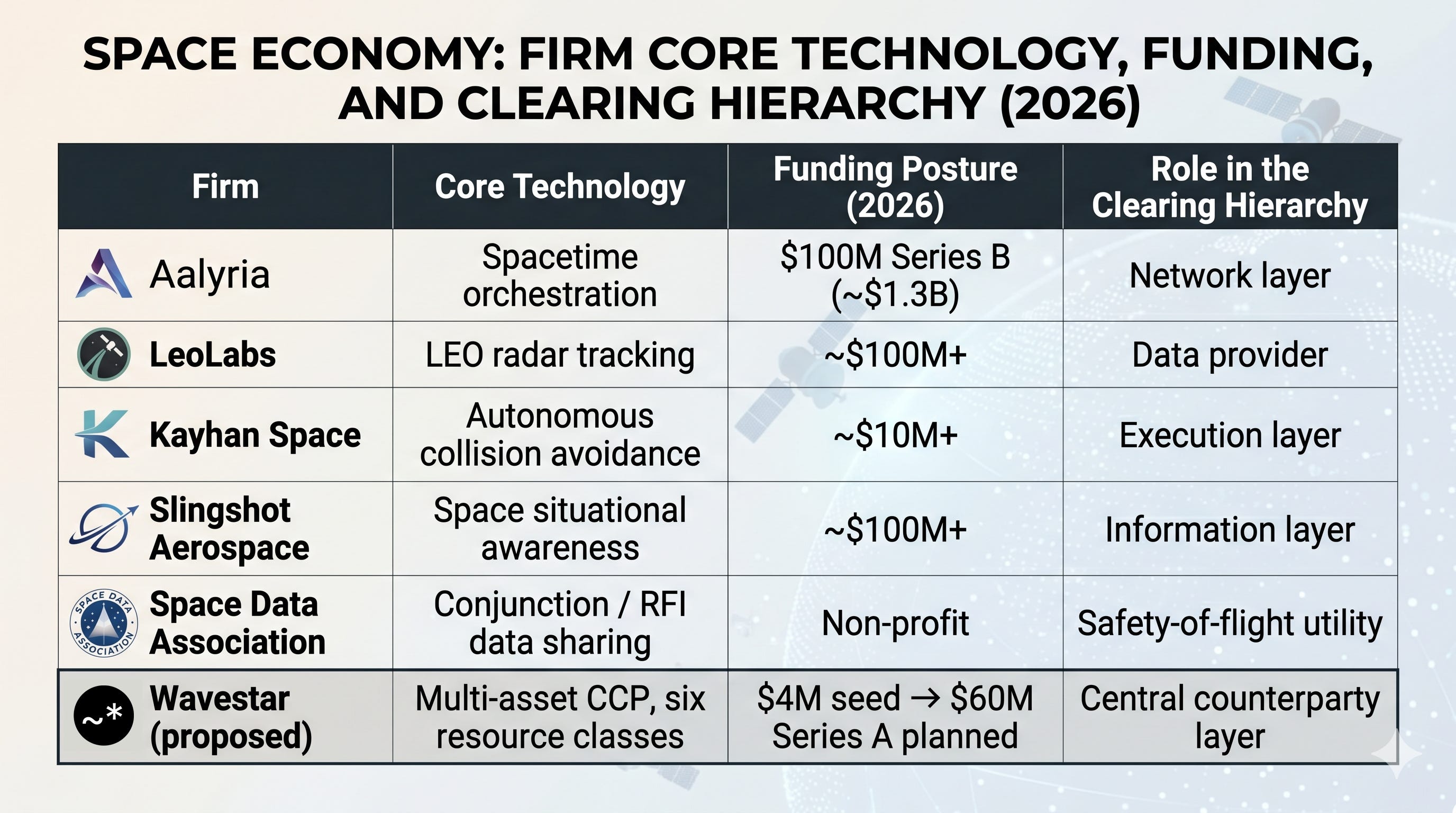

The orbital-orchestration cohort. A growing set of firms is building the technical layer underneath what would be an orbital CCP: Aalyria, with its “Spacetime” orchestration platform, raised a one-hundred-million-dollar Series B at a $1.3 billion valuation in 2026; LeoLabs operates the LEO radar tracking network; Slingshot Aerospace provides space-domain awareness intelligence; Kayhan Space provides autonomous collision avoidance. Each of these is doing serious infrastructure work. None of them is structured as a central counterparty. They produce the data and the orchestration the CCP needs as inputs.

The remaining economic incentive for keeping the bilateral status quo lies with the major space-law practices at firms such as Hogan Lovells and Wiley Rein, whose bespoke negotiation work a CCP would commoditise. That is exactly the same incentive structure that delayed the formation of DTCC by roughly a decade after the 1968 paperwork crisis.

10. The path: how this gets built between now and 2028

Claim: the regulatory path is the binding constraint, and it is approximately 24 months long if run in parallel. The Wavestar v1 launch is targeted for mid-2028. Design partner cohort closes 26 May 2026.

The licensing chain has three sequential federal filings that have to be run in parallel rather than serial.

The first is FinCEN registration as a Money Services Business, governing initial dollar-denominated margin flows and settlement compliance. This filing is the lowest-friction and serves as the entry-level operating licence.

The second is Securities and Exchange Commission designation as an Alternative Trading System, providing a legally compliant secondary market for asset classes that may be classified as securities or as structured asset subleases (hosted-payload tranches in particular).

The third and most demanding is a Form DCO filing with the Commodity Futures Trading Commission, seeking Derivatives Clearing Organisation status under Section 5b of the Commodity Exchange Act, with eventual designation as a Swap Execution Facility or Designated Contract Market. The statutory CFTC review period for a materially complete Form DCO is one hundred and eighty days, but the operational reality of iterative staff reviews, technology validations, system safeguard assessments, and operational presentations consistently extends the comprehensive lifecycle past two years.

Wavestar runs all three in parallel, anchored against a v1 launch in mid-2028. The protocol architecture explicitly allows early-stage commercial networks to clear transaction intents through compliant offshore structures and localised private netting arrangements during the federal validation period, preventing market stagnation while the regulators work. Subpart C election at registration, on the Nodal Clear model, is the structural target.

11. What we are asking for

Claim: this argument needs design partners, working-group participants, and informed dissent. It does not need passive subscribers.

Three concrete asks, in order of operational importance.

One. The 60-day design-partner cohort closes 26 June 2026. If you operate a satellite, a ground-station network, an ISAM service, a hosted-payload platform, a spectrum-coordination group, or an orbital compute service of any kind, and any part of the argument resonates, the cohort is free, SDK-first, under mutual NDA, and structured around your operational priorities; we adapt to your data shape rather than asking you to adapt to ours. Three of the early cohort members are working operators whose names you would recognise. There is room for two more. Email me directly.

Two. The Compute-Hour Working Group convenes Q1 2027. The objective is to publish an open-source technical specification defining the standardised compute-hour resource class. The working group requires participation from enterprise AI infrastructure architects, semiconductor engineers, and space hardware manufacturers to unify performance metrics across varying hardware profiles (NVIDIA accelerators, AWS Trainium, Google TPUs, custom edge processing). Interested participants apply through direct channels.

Three. Informed dissent is more valuable than passive agreement. If you read this and think the Nodal Clear architectural pattern is wrong for orbital, that captive operator-owned clearing is actually better for the industry, that the FCC order is less of an unlock than I am claiming, or that the four-precondition framework is a misreading of clearing-house formation history, send me the disagreement. The Substack comments are open; my email is mitch@wavestar.space; my LinkedIn is https://www.linkedin.com/in/mitchellmclennan/; my X handle is @wavestarspace.

The orbital economy is in the rare position of being able to choose its clearing architecture deliberately, before the major counterparty failure that would force the choice retroactively. The historical lesson is unambiguous. The US securities industry needed Pickard, Goodbody, and a decade of paperwork-crisis chaos before DTC was built. The OTC derivatives market needed Lehman before LCH SwapClear’s design became orthodoxy. The wholesale electricity market needed Enron before the ISO model became uncontroversial. None of these forcing-function defaults was strictly necessary; in each case, the architectural shape of the eventual solution was visible in advance to practitioners willing to look at it.

The orbital economy does not need to repeat that mistake.

Author

Mitchell McLennan is the founder of Wavestar, the neutral clearing and settlement infrastructure for orbital commodities. He was previously SVP, Capital Markets at Gliese Capital, and earlier built out direct carrier billing settlement rails across 280 telecommunications operators at Centili; the same structural pattern of clearing heterogeneous, multi-counterparty resource flows that the orbital economy now needs at scale. Wavestar Holdings LLC is a Wyoming-incorporated entity targeting a public v1 in mid-2028.

Mitchell can be reached at mitch@wavestar.space. Subscribe to this Substack for the next pieces in the series; the planned Part 2 is a deep dive on the FCC 30 April order’s interference-coordination mechanics; Part 3 examines what an orbital default waterfall actually looks like; Part 4 walks through the open-spec did:orbit identity registry.

Sources and verification

Headline references:

Anthropic / SpaceX Colossus 1 deal, 6 May 2026: CNBC, SpaceNews, xAI announcement, Tom’s Hardware, ServeTheHome

SpaceX / xAI acquisition, February 2026: Via Satellite, SiliconReview, Winbuzzer

SpaceX million-satellite FCC filing: SpaceNews, Data Center Dynamics, Introl

Starcloud-1, nanoGPT training, leadership team, Series A: Starcloud company posts, NVIDIA blog, CNBC, Benchmark portfolio disclosures

FCC Report and Order DOC-421308A1, SB Docket 25-157, 30 April 2026: FCC published document, FCC Fact Sheet DOC-420708A1, Via Satellite, SatNews, Inside Global Tech

FCC Chairman Brendan Carr remarks (April 2026 disclosure of $28B bilateral spectrum deal flow): FCC press materials

SEC / CFTC Memorandum of Understanding, 11 March 2026 (Joint Harmonisation Initiative): SEC and CFTC published MOU

Kepler Communications Aether ISL launch, January 2026: Kepler Communications press, SDA optical standards documentation

AST SpaceMobile HALO Europa, February 2026 ($30M prime contract): SDA press, AST SpaceMobile press

Ligado / Inmarsat L-Band Cooperation Agreement and Viasat $770M insurance claim: Viasat investor disclosures, bankruptcy court filings

FCC DISH / EchoStar $2.4B escrow requirement, May 2026: FCC orders

DTCC structure and $2.5 quadrillion 2022 settlement: DTCC corporate disclosures, Marc Rubinstein’s “WTF is DTCC?” (Net Interest)

LCH SwapClear Lehman Brothers $9T unwind: LCH disclosures, post-2008 retrospectives

Nodal Clear Subpart C status, EEX 2017 acquisition, Coinbase Derivatives 2022 clearing: CFTC public records, EEX press, Coinbase press

Novaspace 2026 small-satellite outlook: Novaspace published report

1968-1972 paperwork crisis: SEC 1963 Special Study of the Securities Markets, Goodbody & Co. failure records, NYSE historical archives

FERC Order 888 and ISO buildout: FERC archive, Joskow / Tirole literature

CME weather derivatives volume disclosures: CME quarterly disclosures

Aalyria Series B ($100M / $1.3B): Aalyria press, 2026 funding announcement

Wavestar Holdings LLC. Wyoming. The four preconditions are satisfied. The clearing infrastructure for the orbital economy is the work of the next twenty-four months. Send disagreement; that is faster than agreement.

Originally published on

mitchellmclennan.substack.com